It can also reveal you the overall quantity of interest you" ll pay over the life of your mortgage. To use this calculator, you" ll require the following details: Home price - The dollar quantity you expect to spend for a house. Deposit - The down payment is money you offer to the home's seller.

Home mortgage Amount - If you're getting a mortgage to purchase a new house, you can discover this number by deducting your deposit from the home's price. If you're re-financing, this number will be the impressive balance on your mortgage. Home Loan Term (Years) - This is the length of the mortgage you're considering.

On the other hand, a property owner who is re-financing might choose of a loan that lasts 15 years. Interest Rate - Quote the interest rate on a brand-new home mortgage by examining Bankrate's home mortgage rate tables for your area. When you have a forecasted rate (your real-life rate might be different depending on your overall credit photo) you can plug it into the calculator.

When you look for a home mortgage, you quickly become immersed in a new language. It can all sound very foreign at initially, however we'll condense some basics here about how mortgages work and language that is typically utilized. Initially, let's look at what you truly are paying when you make a home loan payment.

This is what you are paying to obtain the cash for your home. It is computed based on the rates of interest, how much principal is impressive and the time duration during which you are paying it back - how do assumable mortgages work. At the beginning of the loan repayment duration, the majority of your payment actually is going towards interest, with a small portion breaking paying down the principal.

Many house owners will pay their yearly real estate tax in routine increments to the lender (e.g., quarterly). Lenders will need house owners insurance coverage, so a few of your monthly payment will be assigned to your insurance coverage. You sometimes will also need to pay a home loan insurance premium. Taxes and insurance coverage are held in escrow on your behalf.

How Do Mortgages Work For Custom Houses Things To Know Before You Get This

U.S - how do commercial mortgages work.MortgageCalculator.org deals an easy method to see how home loan payments get used to the elements simply described. You can use this calculator (likewise available as an Android app) to plug in numbers for your own home loan. Plug your own numbers in the amortization calculator and scroll down to see just how much you really will pay over the life of your loan.

Try it with the calculator to see how simply including $20 a month can minimize the general expense of your loan repayment.

Getting a home loan is one of the most substantial monetary choices the majority of us will ever make. So, it's vital to comprehend what you're signing on for when you obtain money to purchase a home. A mortgage is a loan from a bank or other banks that assists a borrower purchase a house.

A home mortgage includes two primary elements: primary and interest. The principal is the specific quantity of cash the homebuyer borrows from a loan provider to purchase a home. If you buy a $100,000 house, for example, and borrow all $100,000 from a lender, that's the principal owed. The interest is what the lending institution charges you to borrow that money, says Robert Kirkland, senior house lending consultant at JPMorgan Chase.

Debtors pay a mortgage back at regular periods, usually in the type of a month-to-month payment, which usually includes both primary and interest charges." Monthly, part of your regular monthly home mortgage payment will go towards settling that principal, or home loan balance, and part will approach interest on the loan," says Kirkland.

In such cases, the money collected for taxes is held in an "escrow" account, which the lending institution will use to pay your residential or commercial property tax costs when taxes are due. Homeowners insurance coverage offers you with security in case of a catastrophe, fire or other mishap. Sometimes, a lender will gather the premiums for your insurance coverage as part of your regular monthly home mortgage bill, place the cash in escrow and make the payments to the insurance supplier for you when policy premiums are due.

Everything about How Do Subprime Mortgages Work

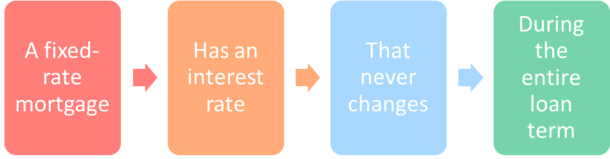

There are a number of kinds Informative post of mortgages available to customers. They consist of conventional fixed-rate mortgages, which are among the most typical, in addition to adjustable-rate home mortgages (ARMs), and balloon home mortgages. Potential property buyers must investigate the right alternative for their requirements. The name of a home mortgage typically indicates the way interest accumulates.

Fixed-rate home mortgages are available in terms varying up to 30 years, with the 30-year option being the most popular, states Kirkland. Paying the loan off over a longer amount of time makes the month-to-month payment more affordable. But no matter which term you prefer, the rate of interest will not alter for the life of the home loan.

Under the regards to an variable-rate mortgage (ARM), the rate of interest you're paying may be raised or lowered occasionally as rates alter. ARMs might a great concept when their rate of interest are particularly low compared with the 30-year fixed, specifically if the ARM has a long fixed-rate duration before it starts to adjust." Some examples of a variable-rate mortgage would be a 5/1 ARM and or a 7/1 ARM," said Kirkland.

Under the regards to a balloon home mortgage, payments will begin low and then grow or "balloon" to a much larger lump-sum amount before the loan ends. This kind of mortgage is generally focused on buyers who will have a greater earnings towards completion of the loan or loaning duration then at the beginning.

For those who do not mean to sell, a balloon home mortgage might require refinancing in order to remain in the home." Buyers who select a balloon home mortgage might do so with the intent of re-financing the home mortgage when the balloon home loan's term goes out," states Pataky "Total, balloon home loans are among the riskier types of mortgages." An FHA loan is a government-backed home loan insured by the Federal Housing Administration." westlake financial services las vegas nv This loan program is popular with lots of novice homebuyers," states Kirkland.

The VA loan is a loan ensured by the U.S. Department of Veterans Affairs that requires little or no money down. It is available to veterans, service members and qualified military partners. The loan itself isn't in fact made by the federal government, however it is backed by a government firm, which is designed to make lending institutions feel more comfortable in offering the loan.

An Unbiased View of How Mortgages Subsidy Work

It is essential to understand as you go shopping for a mortgage that not all mortgage products are developed equivalent, so doing your research study is important, says Kirkland." Some have more strict standards than others. Some lenders might need a 20 percent deposit, while others require as little as 3 percent of the home's purchase price," he says.

In addition to understanding the numerous home loan products, invest some time going shopping around with different lenders." Even if you have a preferred lender in mind, go to 2 or 3 lendersor even moreand make certain you're fully surveying your choices," says Pataky of TIAA Bank. "A tenth of a percent on rate of interest may not look like a lot, however it can translate to thousands of dollars over the life of the loan - how do reverse mortgages work after death.".